What becomes of credit card debt if you relocate overseas without paying it?

If you're considering relocating overseas and leaving behind a large amount of credit card debt, you may be wondering what becomes of that debt and read all the great reviews and articles on FitMyMoney about that.

It can be difficult to say goodbye to family and friends in pursuit of a new life abroad - but even more so when burdened with the worry about how your debt will be handled back home.

As daunting as it might seem, there are certain steps you can take before moving to decrease your chances of being pursued by creditors while also ensuring that your credit stays intact while living abroad.

In this blog post, we'll go through exactly what happens if you do not pay off all existing credit cards prior to relocation and provide some advice on how best to manage them upon emigrating overseas.

What does credit card debt mean for your overseas move

Moving overseas is a big commitment and one which many people take as an exciting opportunity to explore the world. However, low budget travelers must be mindful of their finances and how carrying a high amount of credit card debt can dampen the opportunity significantly.

Credit cards aren’t the only financial burden you should worry about; other factors such as savings, emergency funds, exchange rates, travel expenses, and more all come into play. Yet accumulating credit card debt carries its own set of unique consequences that can keep your abroad adventure from reaching its fullest potential.

For example, if you are unable to make payments on your debt while overseas, then it's likely that your already limited funds will diminish quickly. Furthermore, you may also alienate certain banking institutions, which could make obtaining access to cash even more difficult.

Ultimately, being aware of your current financial situation before the relocation is essential in ensuring you have enough money for your adventure abroad.

Types of debt that can follow you overseas

It's important for global residents to be aware that a certain type of debt remains enforceable even when individuals leave their home country. Namely, student loan debt is one of the most common types of debt that can follow overseas citizens wherever they march along international borders.

Credit cards, auto loans, and mortgages also count among the financial obligations that come with you, no matter your location, so it's critical to have a plan in place to manage any outstanding payments, regardless of whether you're living in New York City or Mumbai.

In some cases, personal debts incurred while abroad may even be collected by foreign creditors using international court systems. Even though debt tends to take on many shapes and sizes, it's important to remember that it is always prudent to stay up-to-date with any financial obligations before they become too hard to handle.

Impact on your credit score and finances when moving abroad

Moving abroad for extended periods of time can have a major impact on your credit score and overall financial health. One of the possible consequences to be aware of is that if you are out of the country for more than six months, it could affect your credit utilization ratio.

This is because creditors may not report your credit activity while you are away from its origin country, meaning that some lenders may stop considering you as a valued customer.

Additionally, depending on which country you move to, you may encounter difficulty in utilizing certain banking services due to regulations and restrictions that can complicate matters further.

It's best to do proper research about local banking services or find alternatives before deciding to move abroad in order to avoid any major financial hiccups as a result.

Do you owe interest during a move abroad?

Relocating to another country can be quite the undertaking, and one of the questions many people ask is: Do I owe interest during a move abroad? The answer to this question varies greatly depending on individual circumstances.

Generally, interest on moving expenses begins to accrue when you become a tax resident in the new host country. If you are working and subject to taxation in your new home base, you will most likely incur taxes for that period and be required to pay any applicable interest due.

You should always consult with a qualified tax consultant regarding moves abroad, as each case is different and differs from country to country. With proper planning, however, it's possible to avoid or curtail interest charges related to a move overseas.

How to deal with unpaid credit card debt when you relocate

If you have unpaid credit card debt but are planning to move, it can be challenging. The best advice to address this issue is to call your credit card company and explain your case; many companies will be compassionate and willing to discuss options with you.

Other solutions include negotiating for lower payments or creating a debt repayment plan. Additionally, if you are relocating out of state, always ask what options the bank has for handling any remaining balance when leaving the area.

Being proactive and reaching out to creditors with an honest conversation about what you can reasonably pay and how long it will take is usually the most effective approach for dealing with unpaid credit card debt when relocating.

What you need to know about bankruptcy and relocating overseas

Bankruptcy is a complicated financial situation that becomes even more complex when relocating overseas. It's important to weigh your options before deciding whether or not to pursue bankruptcy if you're contemplating international relocation.

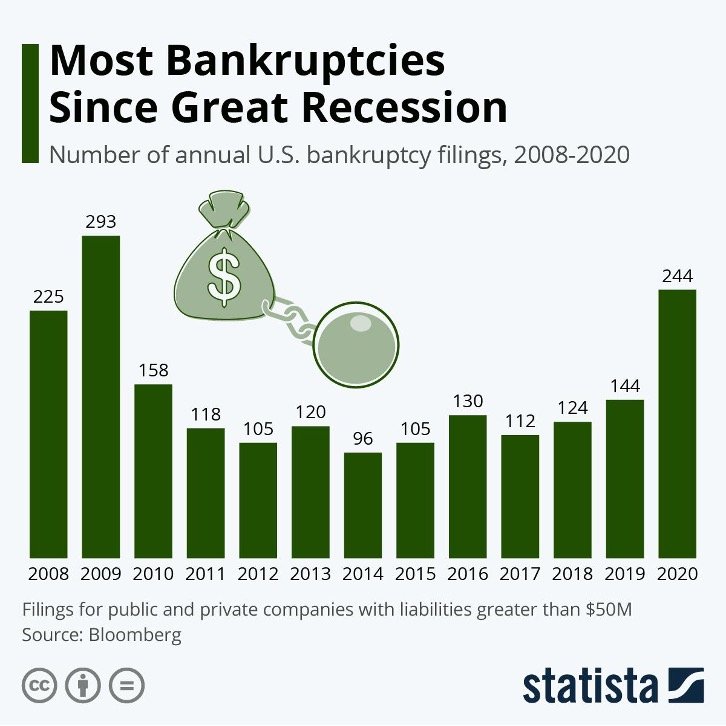

According to the survey, 2020 was a historic year for bankruptcies in the US,, with more large companies filing than at any other time since the Great Recession of 2009.

Banks, investments, and real estate businesses were among those hardest hit by this recessionary period, yet similar to what occurred during the pandemic, bankruptcies impacted many different industries over a wide area.

Depending on the laws of the country you are moving to, filing for bankruptcy may not be possible there because some countries do not recognize certain debts. Additionally, if you owe back taxes in the US, creditors can seize any foreign assets if these debts remain unpaid.

This can make attempting to move abroad difficult without some form of debt resolution. Understanding these nuances is paramount for anyone looking to navigate circumstances like these overseas successfully.

Conclusion

Moving overseas can be an advantageous experience and one that opens up a world of possibilities. However, there are potential financial obstacles to look out for before relocation.

For those with credit card debt, it's essential to have a plan in place, as this type of debt may follow you across the border and have an influence on your finances after the move.

Interest will likely continue to accrue until the balance is paid off too. Working with creditors or debt collectors may be necessary at first, but if necessary, filing for bankruptcy is also an option to consider.

Ultimately, being informed about what debts are possibly portable and how to handle them when relocating can help ensure a smoother transition overseas and more financial stability in the new country.