Gift cards are becoming a core payment layer in global retail

Gift cards used to sit at the edge of retail strategy. They were seasonal products, last-minute presents, or loyalty incentives handed out during promotions. Today, they are becoming something more important: a flexible payment layer that helps connect consumers, merchants, wallets, marketplaces, and cross-border commerce.

As global retail becomes more fragmented, gift cards are increasingly acting as a bridge between different payment systems. They allow consumers to move value into retail ecosystems without always relying on traditional card payments, bank transfers, or local payment methods.

From Gift Product to Payment Infrastructure

The old view of gift cards was simple: a customer bought a card, gave it to someone else, and the recipient spent it with a specific retailer.

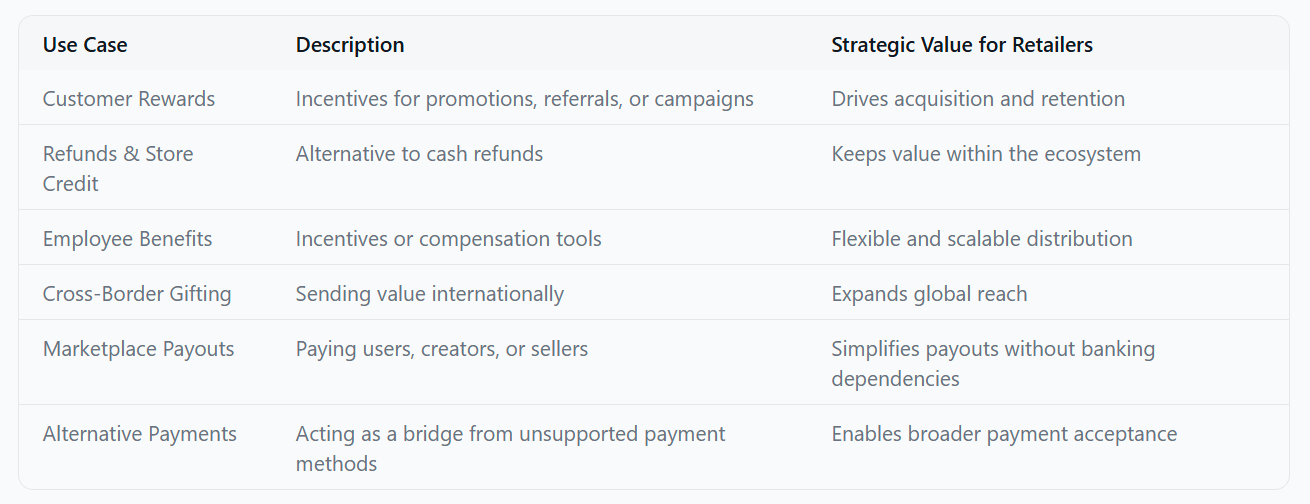

That model still exists, but digital commerce has expanded the role of gift cards. They are now used for a wide range of functions across the retail ecosystem.

In many cases, the gift card is no longer the end product. It is the mechanism that enables a transaction.

Why Retailers Like the Model

For retailers, gift cards offer several structural advantages. They are prepaid, closed-loop, and relatively easy to distribute digitally. That makes them attractive in markets where payment acceptance is complicated, expensive, or fragmented.

Instead of directly integrating every emerging payment method, retailers can rely on partners and platforms that distribute digital gift cards globally. This allows them to access demand without increasing operational complexity.

The Cross-Border Retail Challenge

Cross-border retail is often limited by payment friction. A customer may want to buy from a retailer, but their preferred payment method is not accepted. Their card may fail. Bank transfers may be too slow. Local wallets may not be supported internationally.

Gift cards create an alternative route.

Instead of forcing every retailer to support every local payment method, gift card distribution can sit between consumer demand and merchant acceptance. This is especially useful for global brands that already have strong demand but limited localized payment support.

Crypto Makes the Use Case More Visible

One of the clearest examples of this shift is crypto funded retail spending.

Many consumers hold digital assets but still face friction when trying to use them in everyday commerce. Direct crypto checkout is still not widely adopted across global retail.

Gift cards provide a practical workaround.

Platforms like CoinsBee enable users to convert crypto into real-world purchasing power. Through services such as online shopping with crypto, customers can access thousands of brands globally without requiring those brands to directly accept crypto payments.

This model removes complexity for retailers while unlocking demand from crypto-native consumers.

Gift Cards as an Abstraction Layer

In technology terms, gift cards function as an abstraction layer between payment methods and merchants.

Consumers can fund purchases using one system, while retailers receive value through another. This reduces integration complexity and allows both sides to operate within their preferred environments.

This abstraction is increasingly important as the payment landscape continues to fragment across:

Cards

Bank transfers

Digital wallets

Loyalty systems

Crypto assets

Regional payment networks

Retailers cannot integrate everything. Consumers expect flexibility. Gift cards help close that gap.

Benefits for Consumers

For consumers, digital gift cards offer convenience and flexibility. They can be delivered instantly, used globally, and funded through various payment methods.

They are particularly useful for:

International shoppers

Crypto users

Users without access to certain banking systems

Participants in loyalty or rewards ecosystems

Gift cards reduce friction between stored value and actual spending.

Benefits for Retailers

For retailers, gift cards represent more than just a product. They are a scalable infrastructure layer for growth.

Key benefits include:

Access to new customer segments

Incremental prepaid revenue

Reduced need for complex payment integrations

Participation in global distribution networks

Increased conversion in markets with payment friction

This is why gift cards are increasingly treated as part of payment strategy rather than just merchandising.

The Role of Marketplaces and Wallets

Wallets, exchanges, neobanks, and marketplaces all hold customer balances that need real-world utility. Gift cards provide a fast and scalable way to convert those balances into retail spending.

Platforms like CoinsBee play a key role in connecting these ecosystems. They enable seamless distribution of retail value across different payment environments, benefiting both platforms and merchants.

Challenges Still Remain

Despite their advantages, gift card systems must address several challenges:

Fraud prevention

Regional restrictions

Pricing transparency

Customer support

Brand control

A poor experience can quickly erode trust, making reliability and transparency critical.

What Comes Next

The evolution of gift cards will likely focus on infrastructure and integration rather than the product itself.

Future developments may include:

API-based distribution systems

Deep integrations with wallets and exchanges

Real-time inventory and pricing

Embedded checkout experiences

Personalised incentives and rewards

Conclusion

Gift cards are no longer just a gifting product. They are becoming a core payment layer in global retail.

They enable consumers to spend value across ecosystems, help retailers access new demand without added complexity, and allow platforms to turn stored value into real-world utility.

In a fragmented payments landscape, this makes gift cards strategically essential. Platforms like CoinsBee demonstrate how this model can scale globally, bridging the gap between emerging payment systems and everyday retail.