How retailers are bringing payments into the customer journey

Payment infrastructure used to live in the background, a back office concern handled by finance teams and technology vendors, largely invisible to the customer. That is no longer the case. Across UK retail, the way money moves has become a front-of-house priority. Checkout experiences now directly influence brand perception, basket size, and repeat purchase behaviour.

The change is being driven by integrated financial services. This includes integrating payments, credit, and loyalty programmes directly into the shopping experience. Rather than operating as separate services, they form part of a single customer journey. For retail professionals, understanding this change is no longer optional. It is one of the defining infrastructure challenges of the decade.

Retail Payments Are No Longer Back Office

For much of the past two decades, retailers treated payment processing as a utility, something that had to work reliably but did not need to be a point of differentiation. The rise of ecommerce began to change that, as online retailers competed on checkout speed and simplicity. Now those expectations have migrated into physical stores, quick-service restaurants and subscription-based retail models alike.

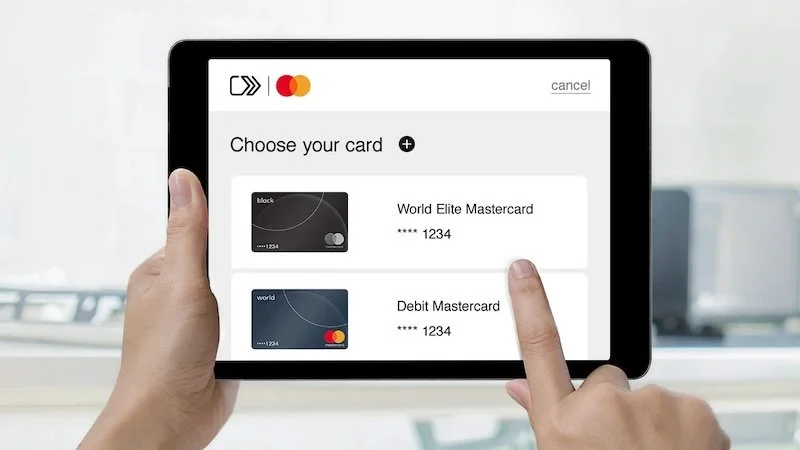

Mobile wallets are a clear indicator of how quickly consumer habits have changed. Mobile wallet adoption reached 57% of UK adults in 2024, up from 42% the previous year, a 36% year-on-year increase. That is a structural change in how British consumers expect to pay, and retailers who do not accommodate it risk losing transactions to competitors who do.

Card Infrastructure Meets Consumer Expectation

Cards remain the foundation of UK retail payments, but what "paying by card" actually means has changed considerably. Contactless, tokenised and wallet-accessed card transactions are now the norm, not the exception.

The physical card handed over at a terminal is increasingly an abstraction of a stored credential used across multiple devices and channels. Nowhere is this more visible than in digital-first sectors where frictionless card-based payments have been standard for years.

For example, gambling platforms like credit card casinos in the UK offer a clear illustration of how mature card-based infrastructure looks in highly competitive digital environments. Instant deposits and smooth transaction flows are the baseline expectation rather than a premium feature.

UK retail is arriving at the same destination, driven by the same consumer instincts. According to a Rapyd UK payments overview, 94.6% of all eligible in-store card transactions in the UK were made contactlessly in 2024. This shows just how thoroughly consumers have embraced low-friction card payment as their default behaviour.

How Other Digital Sectors Set the Benchmark

Digital platforms have consistently outpaced physical retail in delivering effortless payment experiences. The consumer expectations formed in those environments do not disappear when someone walks into a shop. The result is a rising benchmark that retailers must now meet across every channel they operate.

The commercial consequences of failing to meet that benchmark are tangible. Research found that 43% of shoppers would pay more for a product if the overall experience were more convenient.

Convenience is not a nice attribute; it is a direct lever on revenue. Retailers who invest in integrated, low-friction payment flows are not just improving customer satisfaction. They are making a measurable commercial argument for that investment.

The same research indicates that 55% of consumers are comfortable using self-checkout, and 34% already use scan-and-go or self-scanning in stores. These numbers reflect a population that has internalised autonomous, tech-enabled payment as the preferred model, and will gravitate towards retailers who deliver it.

Embedded Finance Becomes a Competitive Differentiator

Buy Now, Pay Later and card-linked instalments is the next phase of this infrastructure evolution. BNPL has moved well beyond niche fintech positioning.

UK BNPL transaction value reached approximately £13 billion in 2024, with one in five UK adults using such services over a 12-month period. The technology is now a standard line item in the checkout decision for a substantial portion of the adult population.

Retailers who treat integrated finance as an infrastructure decision are positioning themselves to compete on the terms that consumers already expect. The plumbing is becoming the product.