The rise of license marketplaces: how FinTech companies are accelerating market entry

Launching a FinTech company has never been easier from a technology perspective. Cloud infrastructure, Banking-as-a-Service providers, white label platforms, and API driven ecosystems allow founders to build sophisticated financial products faster than ever before.

However, technology is no longer the primary obstacle. For many FinTech, payments, and crypto businesses, regulatory access has become the real challenge. Obtaining a financial license can take months or even years depending on the jurisdiction, while regulatory expectations around compliance, governance, AML controls, and risk management continue to increase.

As a result, a new segment of the fintech ecosystem is gaining momentum: license marketplaces. These platforms connect buyers with existing regulated entities and licensed businesses, creating alternative pathways for companies seeking faster market entry.

Why Traditional Licensing Has Become a Bottleneck

Financial regulation plays a critical role in protecting consumers and maintaining the integrity of the financial system. However, the licensing process itself can create significant barriers for growing businesses.

Many founders underestimate the resources required to obtain a financial license. Beyond application fees, businesses often need to establish compliance frameworks, appoint qualified personnel, implement AML procedures, prepare extensive documentation, and maintain ongoing regulatory reporting.

The challenge becomes even greater for companies expanding internationally. Entering multiple jurisdictions may require separate licensing processes, local directors, regulatory consultations, and jurisdiction-specific compliance programs.

For startups operating in highly competitive markets, waiting 12 to 24 months for regulatory approval can create a substantial opportunity cost. During that period, competitors may launch similar products, secure partnerships, or capture market share.

This reality has encouraged many companies to explore alternative market entry strategies.

The Emergence of License Marketplaces

License marketplaces have emerged as a response to increasing regulatory complexity and growing demand for faster expansion.

Rather than starting the licensing process from scratch, companies can explore opportunities to acquire existing regulated entities, licensed businesses, or corporate structures that already possess the necessary regulatory permissions.

The concept is not entirely new. Mergers and acquisitions have long been part of the financial services industry. What is changing is the accessibility of these opportunities. Specialized marketplaces now make it easier for FinTech founders, investors, and financial institutions to discover regulated entities that align with their strategic objectives.

These marketplaces typically focus on regulated businesses operating in payments, money services, electronic money, digital banking, foreign exchange, and digital asset sectors.

Importantly, acquiring an existing regulated structure does not eliminate compliance obligations. Regulatory requirements continue to apply after acquisition. However, it may significantly reduce the time required to establish a regulated presence in a target market.

Types of Licenses Commonly Available Through Marketplaces

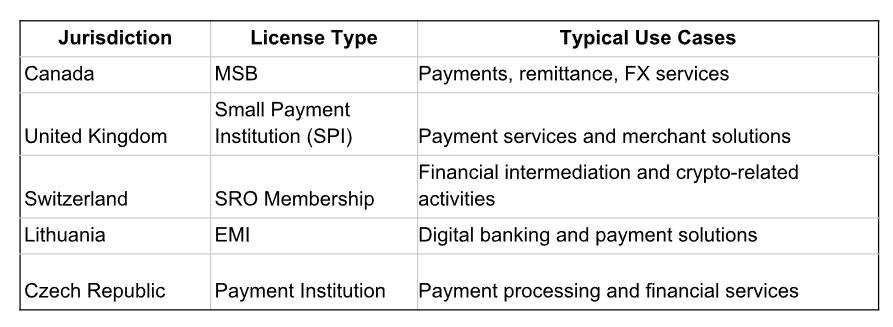

The market for regulated entities has expanded significantly in recent years. Depending on the jurisdiction, businesses may find opportunities involving various license categories.

Among the most frequently requested options are a Canadian MSB, which provides a recognised framework for money services businesses operating in payments, foreign exchange, and remittance activities.

For companies seeking accelerated market entry, acquiring a Canadian MSB for sale may offer a faster alternative compared to starting the licensing process from the beginning, subject to regulatory, legal, and operational due diligence.

Why Investors and Fintech Founders Are Paying Attention

The growing interest in license marketplaces is driven by several practical considerations.

Faster Market Entry

Speed has become one of the most valuable competitive advantages in FinTech. Companies that can launch products faster are often better positioned to capture customer demand and establish partnerships before competitors enter the market.

Acquiring an existing regulated structure may significantly reduce the timeline required to begin operations in a new jurisdiction.

Existing Compliance Foundations

Many regulated entities already have established compliance policies, AML procedures, internal controls, and operational documentation.

While these frameworks frequently require updates following acquisition, they can provide a foundation that reduces implementation efforts.

Established Business Relationships

Some regulated entities maintain existing relationships with banks, payment providers, technology vendors, auditors, or compliance partners.

Although these relationships are not guaranteed to transfer seamlessly, they can offer valuable operational advantages during expansion.

Reduced Execution Risk

Starting from scratch involves numerous uncertainties. Licensing timelines may change, regulatory expectations may evolve, and application outcomes are never guaranteed.

Acquiring an existing regulated structure can help reduce certain regulatory and operational uncertainties.

Capital Efficiency

Building a licensed operation often requires significant investment before revenue generation begins. For some companies, acquiring an existing entity may represent a more efficient allocation of capital compared to lengthy licensing projects.

Not Every Licensed Entity Is Equal

Despite growing interest in license marketplaces, buyers must approach acquisitions carefully.

A regulated entity's value extends far beyond the license itself. Its operational history, compliance record, ownership structure, banking relationships, and regulatory standing all contribute to its attractiveness.

Comprehensive due diligence should include legal, financial, operational, and compliance assessments. Buyers should evaluate regulatory correspondence, historical audits, AML programs, corporate records, ownership structures, and any outstanding obligations.

An entity with unresolved compliance issues may introduce significant risks that outweigh any potential time savings.

This is why professional advisory support remains essential throughout the acquisition process.

How Technology and Licensing Are Converging

One of the most important developments in the FinTech industry is the convergence of licensing and technology infrastructure.

Historically, obtaining a license and building a technology platform were treated as separate projects. Today, businesses increasingly seek integrated solutions that combine regulatory access with operational readiness.

Companies are no longer looking solely for a regulated entity. They are looking for a complete ecosystem that may include payment connectivity, compliance tooling, customer onboarding systems, transaction monitoring, core banking capabilities, digital wallets, card issuing, and reporting infrastructure.

This shift has created demand for marketplaces that offer both regulatory opportunities and operational solutions.

As a result, buyers increasingly evaluate licensed entities not only on regulatory status but also on their ability to support scalable financial products.

The Future of Fintech Expansion

The evolution of license marketplaces reflects a broader transformation within financial services.

Just as cloud computing reduced the need to build physical data centres, new marketplace models are reducing the barriers associated with entering regulated markets.

Over the coming years, FinTech companies are expected to increasingly combine ready made regulated structures, Compliance-as-a-Service providers, white label banking platforms, embedded finance infrastructure, and specialised technology partners to accelerate growth.

The focus is shifting from building every component internally toward assembling highly specialised ecosystems that enable faster execution and greater flexibility.

Conclusion

License marketplaces are not replacing financial regulation. Instead, they are changing how businesses gain access to regulated markets.

As regulatory requirements continue to grow and competition intensifies, FinTech companies are searching for faster and more efficient ways to expand internationally. Existing regulated entities, when properly evaluated and supported by strong compliance frameworks, can provide a valuable pathway to market entry.

For founders, investors, and financial institutions pursuing growth opportunities across multiple jurisdictions, license marketplaces are becoming an increasingly important component of modern expansion strategies.